In winter 2010, I took a class at the University of Michigan (ENGR 520: Entrepreneurship for Engineers and Scientists). During this class, three colleagues (Jinyong Kim, Corey Kosch, and Joanna Widjaja) and I formed the Health Care Diagnostics Group and write the following report as part of the class project.

I. Introduction

The goal of this work is to analyze the value chain and explore the opportunities to launch a venture capitalist’s back-able firm within the health care industry. Within the health care industry we are focusing on diagnostics, and within diagnostics we are focusing on cardiac monitoring space. This report should be useful for guiding entrepreneurs interested to launch new ventures in the cardiac monitoring space.

This report will start by defining the opportunity space. The value chain of cardiac monitoring space will be described in detail in section II and it will be shown that the cardiac monitors manufacturing segment is capturing the most value. This section will also describe what the manufacturing segment does and who their customers are. In section III, Porter’s five forces of this industry (manufacturing) will be discussed. Sections IV and VI will further discuss Mullin’s framework by analyzing the micro- and macro- market, and micro- and macro- industry, respectively. In section V, the proposed solution (iNurse) will be described in further details. Financial and venture analysis for our proposed firm as well as conclusion will be addressed in section VII.

The opportunity space – Cardiac Monitoring Systems:

Cardiovascular diseases (CVD) are one of the leading causes of death1. Billions of dollars are being spent on the diagnosis, treatment and rehabilitation of patients with cardiovascular diseases. There are two main reasons for the rise in incidence of these life-threatening diseases: (1) Faulty lifestyles and (2) the ageing baby boomer population. Under these circumstances, cardiac monitoring and diagnostics systems enable effective diagnosis and therapy; and thus tend to find substantial application in hospitals and cardiac centers. Hence, enhanced emphasis on the monitoring of cardiovascular diseases to facilitate prevention and early treatment is expected to propel growth in the diagnostic cardiac monitoring systems market2.

Cardiac monitoring generally refers to continuous electrocardiography with assessment of the patients’ condition relative to their cardiac rhythm3. Cardiac monitoring and diagnostic services help physicians to reach accurate and timely decisions in the diagnosis of various forms of CVD. The major types of cardiac monitors are those used in critical care units (bedside monitors), for clinical uses (Electrocardiogram units), and those used for long-term recording (Holters)4.

II. Cardiac Monitoring Value Chain

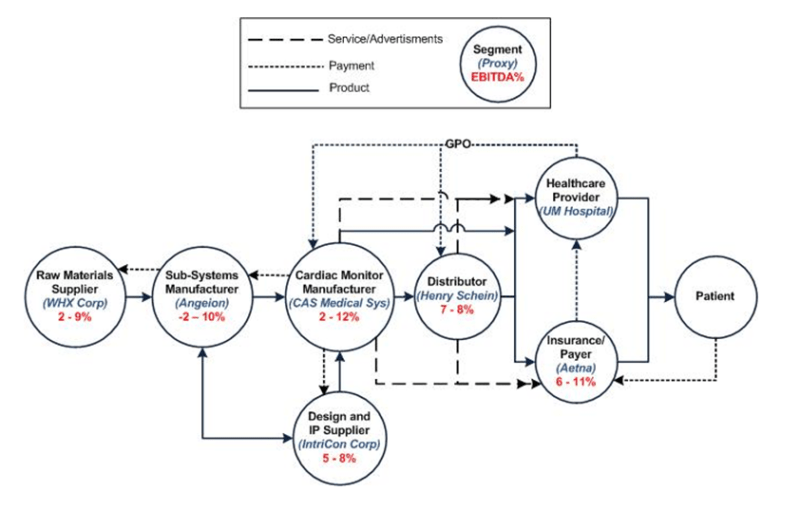

Figure 1. Value Chain for Cardiac Monitors

This space includes segments such as design, manufacturing, and distribution of systems or subsystems that would finally result in a device that can monitor the cardiac activity of patients through healthcare providers. As shown in figure 1, the major segments of this space are raw material suppliers, subsystems manufacturers, cardiac monitors’ original equipment manufacturers (OEMs), Design and IP suppliers, distribution, and insurance companies.

The value chain starts with raw material suppliers that usually serve multiple segments in different value chains. One example of this segment is WHX Corporation which supplies precious metal, tubing, and engineered materials to many industries including healthcare industry 5 . Precious metals are required for the fabrication of electrocardiogram (ECG) electrodes. This segment supplies basic materials and components to cardiac monitor subsystems manufacturers. This segment includes manufacturers of sensors (e.g ECG lead wire), electronic modules and printed circuit boards (PCB), software, and other electrical and mechanical subsystems that ultimately goes into cardiac monitors OEMs. An example of this segment is Angeion Corporation that sells cardiorespiratory diagnostic subsystems for wide range of applications in healthcare to medical device manufacturers, clinical research organizations and others 6 . There is also another segment that supplies design and intellectual property (IP) to cardiac monitors OEM. A company such as IntriCon Corporation falls into this segment that is engaged in the design, development, engineering and manufacturing of electronic products and body-worn devices3. As shown in figure 1, the cardiac monitor OEM segment captures relatively the highest value in the chain. A proxy company for this segment is CAS Medical Systems Incorporation (CASMED). CASMED designs, manufactures and markets critical care cardiac monitors, vital signs monitors, and cardiac output monitors 7 . The companies in this segment usually distribute their products to healthcare providers either directly or through distributors such as Henry Schein Incorporation. However, manufacrurers of specialty devices, such as cardiac monitors, typically have not used large distributors for their products 8 . The main reasons for that are: (1) the major missions of manufacturers is to have direct contact with clinicians (unimpeded by intermediaries), (2) the manufacturer posseses critical knowledge about product features and uses the help to satisfy customer needs, while most distributors lack in-depth product knowledge, and (3) there may be insufficient customer demand for many specialty items. Another important segment in this value chain is the insurance companies (payers). OEMs and distributors also sell their products to insurance companies such as Aetna Incorporation. The figure above shows also the advertisement, service and payment flow in addition to product flow within the cardiac monitor value chain.

The EBITDA margin of the cardiac monitoring manufacturing segment shows that it is really an attractive industry to launch a new business.

The Manufacturing Segment of Cardiac Monitoring Systems:

This segment manufactures resting ECGs, stress testing systems, ECG data management systems, Holter monitor systems, and cardiac event monitoring systems9 . This segment is also concerned about:

- • Product design and manufacturing: There is a huge range of product offers from this segment that varies from massive machinery to portable patient care devices and even some implantable versions. In general, the machinery and devices manufactured are geared for either in-hospital care, outpatient care or both, for patients ranging from adults to pediatric and neonatal. The device helps to monitor patients’ vital signs, detects irregularities and records all these data.10 11

- • Technical support and training of personnel: The manufacturing segment provides technical support to users and training to medical personnel to ensure proper use of their products. This could be done via instruction manuals, web instructions, phone hot-line or direct training sessions.12 13

- • Servicing and maintenance support: Massive machinery requires consistent maintenance and this service is provided by the manufacturing segment too. In case a product is faulty, the user could also approach the manufacturer to either repair it or return it.14

- • Markets, sells and maintain customer awareness with new technology and best practices15

This segment competes mainly on the basis of five dimensions: (1) product innovation, (2) product performance, (3) pricing and contracting, (4) costs of goods sold, and (5) customer support services.

III. Porter’s Five Forces Analysis of Cardiac Monitoring Manufacturing

Industry Competitiveness

The rivalry within this segment is high to moderate. Larger firms within this segment desire to increase their market share, they are doing this by merging with and acquiring other firms, and building their brands. 16 Mergers and acquisitions create larger firms that are able to exploit economies of scale and drive down their prices. 17 Larger firms can also afford the increasing R&D costs associated with companies that deliver new and improved products. 18 This is especially important in cardiac monitoring manufacturing; new technologies make diagnostic and monitoring work more efficient, thus reducing the number of staff work hours required. 19 This is extremely attractive to hospitals as it reduces overall costs. Brand building has forced firms to distinguish themselves based on qualities other than price, however, healthcare products are mostly commoditized and need to meet standards, leaving very little to distinguish them by, thus most of the competition between firms is still focused on price. For example, Lantheus had to provide more competitive pricing so that its Cardiolite Kit remained in competition with Covidien’s ANDA Kit. 20 However, as industry concentration increases, rivalry tends to decrease via various agreements. 21

Bargaining Power of Suppliers

The supplier power in this segment is moderate. Many suppliers are larger, and some of them are the sole provider of certain components. 22 However, most component pieces are not very useful on their own and need to be incorporated into a larger design; this promotes a partnership between the supplier and manufacturer. 23 Also, some manufacturers vertically integrate their production process by acquiring smaller supply companies. 24

Bargaining Power of Buyers

Buyers display a moderate degree of power. The small number of buyers in this segment gives the buyers more power; the smaller number of buyers forces the manufacturers to compete for their purchases. 25 The buyers in this segment also form purchasing agreements with other buyers, strengthening their power position. 26 The possibility of nationalized health care in the US could reduce the number of buyers even more, and give a lot of power to the government on pricing. 27 Also, due to e-procurement systems, buyers are becoming more and more knowledgeable about the products they are purchasing, driving price competition between manufacturers. 28 All of these arguments show that buyer power is strong, however, the market has traditionally shown that sellers have typically dictated prices, with high profits commonplace. 29 Also, product quality and reliability is highly important in this market, which reduces buyer power to an extent. 30

Threat of New Entrants

The threat of new entrants is moderate. Although brand identity is becoming more important, it still does not carry a lot of weight as most customers are concerned with price and quality. 31 Also, decent market growth and substantial investments from venture capitalists makes this market attractive to enter into. 3233 However, intellectual property rights, regulatory approval, technology licensing, and expensive clinical trials are a large barrier for new companies to overcome. 34 Also, established manufacturers form partnerships to help each other innovate and provide complementary assets to each other, making it difficult for new players to enter. 35

Threat of Substitutes

The threat of substitutes is weak in this segment because most innovation is done iteratively by established companies. 36 However, recent trends show established companies are creating different solutions for the same problems. For example, imaging companies have been competing furiously to produce the most reliable diagnostic-quality CT angiograms. Yet, Toshiba is going after whole-heart imaging in one scan, Siemens is addressing temporal-resolutions limitation with dual source CT, GE has the new snapshot pulse technology and Phillips is working on new detectors and dual-energy imaging.

In conclusion, we believe that the Cardiac Monitoring Manufacturing segment is an attractive segment to launch a startup, especially if one already has non-dependent intellectual property (IP). The interest of venture capitalists in cardiac monitoring startups and the importance placed on quality over brand will make it easier to enter as a new entrant. The current trend in the market to acquire smaller companies is actually beneficial to startups that enter this segment because it shows that an exit through purchase from a larger company is likely.

IV. Micro- and Macro- Market (Mullin’s part 1)

Customers of The Cardiac Monitoring Manufacturing Segment:

We want to understand first of all how the purchasing procedure occurs. The purchasers from the OEM segment are: group purchasing organizations (GPOs) and wholesalers/distributors. GPOs purchase the products on behalf of hospitals, and distributors take title to them and deliver them37 . Typically, the process is initiated by the customer (physician), who submits product requests to the system’s materials and procurement manager, who then selects the items from a product catalog (increasingly electronic). The order is then transmitted to the GPO and distributor for fulfillment. These orders are then bundled and transmitted to the manufacturers for shipment.

Given the complexity of the flow described, there are multiple customers. Hospitals, health care systems, and nursing homes are the ultimate institutionally based customers since they pay the bill for the products that are manufactured and distributed. Within these institutions, however, there are multiple customers who are responsible, directly or indirectly, for ordering the products. According to [38 ], when asked who their customer was, many manufacturing executive joked, “Whoever is on the phone”, or “The person who has a purchase order”. In a more serious vein, they stated they have to “cover all the bases” and consider each of the individuals aforementioned their customer.

Physicians are the end customer for many types of products, especially devices (in our case: cardiac monitor). Their preference must be taken into account for several reasons: (1) At minimum they may complain to senior executives if their preferences are not acknowledged, (2) at maximum, they may decide to take their patients and elective procedures elsewhere if they are dissatisfied. As physicians receive more information around around “best practices” from manufacturers, they may be more willing to make decisions that alter the product type they use. In this manner, manufacturers hope to shape customer demand for clinical preference items. Physicians are also key customers in both hospital-based and freestanding alternate delivery site, such as outpatient centers.

Distributors and GPOs are not generally considered to be customers in the supply chain. They are viewed more as partners for both upstream and downstream players, as well as influencers of what the customer actually purchase.

In conclusion, we will narrow down the customers of the manufacturing segment mainly to physicians and nurses. In section IV of this report we will further classify personas. In the following section, the porter analysis is further discussed to explain why manufacturing (OEM) of cardiac monitors captures relatively high value.

What are some of the challenges faced by the customers?

- • Price Transparency: There is a need to address pricing policy and disclosure, as sellers in this segment operate in oligopolistic markets where not all buyers pay the same price for a given or similar product. Some sellers of devices even have designed contracts accompanying sales agreements that include language forbidding buyers from disclosing the negotiated price to other buyers, or even to patients or insurers, reflective of their market power.

- • Diagnostic is not Therapeutic: In this segment, it is challenging to manufacture diagnostic devices as diagnostics are not priced as high as therapies. Also, reimbursement agencies are unwilling to pay high up-front costs to implant a diagnostic device that provides uncertain benefits in an uncertain amount of time.39 Buyers rate products by measuring how much it helps the patients, and unfortunately, monitoring devices are unlike a pacemaker, which both monitors the heart and delivers therapy when necessary; pacemakers provide a direct benefit to the user 40 . However, due to the recent goal set by Medicare to reduce heart failure hospital admissions by 20% by 2012, many physicians are looking to implantable diagnostic devices for the information necessary to help them keep their patients healthy .

- • Regulation Levels: This industry is highly regulated by FDA. The products require formal clinical studies to demonstrate safety and effectiveness. The trend of regulation is increasing. Manufacturers have to abide by the rules and this causes challenges in their design and manufacturing work.

- • Level of Technology Change: Innovation and product development is the most important source of growth within the industry. This allows the first movers to earn above the average profits for a period of time41 . Continuous product innovation increases the applications for which products can be used, increasing the demand for these products. Some of the features manufacturers compete for are speed in performance, portability, power-use and mobility. Hence, manufacturers have to keep abreast of the newest technology and R&D done by competitors to have a leading edge in their product.

- • Disparity between Buyers and Users: The purchasing process in hospitals is unlike other industries. Products are often ordered by workers on the front line of health care delivery such as physicians, nurses, and so on. Products are ordered in a way that maximizes their availability when needed, rather than minimizes the costs of holding inventory. Moreover, the end user ordering products is not typically the buyer (that is, paying for the product). Product demand is thus based heavily on the clinical preference of physicians rooted in their medical training, not on any formal cost-benefit analysis or budgetary constraint. this attitude may still be part of the culture and mentality of older generations of practitioners. Business practices have crept into the system incrementally over time and have encountered strong resistance from professional norms of patient care and provider autonomy, as well as public goals regarding patient access and quality of care. Thus, professional training in procurement and logistics has never been a hallmark among providers, given the prominent role of clinicians and their preferences for branded items. The contradiction between physician preference and purchasing department efforts for standardization makes this an administrative challenge for manufacturers.42

In general this segment (manufacturing) competes mainly on the basis of five dimensions: (1) product innovation, (2) product performance, (3) pricing and contracting, (4) costs of goods sold, and (5) customer support services43.

The target market we serve as aggregated into personas:

| Alicia Stones | Alicia is a nurse in the Emergency Room (ER) department. She is very time-consciencious, wants to know accurate data fast and is easily-stressed if diagnostic devices do not work efficiently, as there is no room for mistakes in the ER. There are times she wishes for devices that could monitor multiple vital signs simultaneously, and is portable and mobile. As humans tend to err, sometimes she also wishes for a device that could automatically detect irregularities, and provide treatment if needed. |

| Dr. Brock Jones | Dr. Jones works in the Cleveland Clinic (Cardiology specialist) and he has patients that need to move freely while in care. He is enthusiastic about state-of-the-art technology and loves exploring cutting-edge devices. He also finds data tracking and management useful in his assessment work, and prefers convenient, easy-to-use products. Sometimes he is concerned about enhanced accuracy of data collection by means of implantable devices that monitors severely-ill patients wherever they are. |

| Jennifer Grant | Jennifer is a senior nurse in the Intensive Care Unit (ICU). Her daily duty includes monitoring of patients’ conditions and providing defibrillation when needed. Thus, she appreciates devices that could monitor multiple vital signs and deliver automatic defibrillation via programmability. She also wants devices to be user-friendly, have easy data manageability and prefers less “cabling” of patients. |

| Icabod Shahid | Icabod is a paramedic in the Ambulatory department. When handling a patient in an ambulance, he prefers less “cabling” of patient and needs to keep in touch with physicians and nurses. He does this by continuously sending data to a central station, with a physician who is able to instruct him on what to do next. Because of the nature of his work, he requires also mobility. He also wants automatic defibrillation when patients suffer ventricular fibrillation to ensure patients survival rate. |

| Dr. Harie Yacabo | Dr. Yacabo is an operating surgeon at Mayo Clinic Operation Room (OR). He does open heart surgeries and requires supporting devices that he could program to accomodate his sophisticated procedures and record certain heart episodes. He prefers devices that shorten the time between diagnosis and surgical procedures required, with as accurate data as possible. After a surgery, he finds reviewing patients data and surgical reports to be useful for his personal improvement. Patient mobility is not important to him. |

| Martina Shingles | Martina is a senior citizen who suffers from cardiac arrythmia (Home-monitoring and Outpatient). Physicians recommend that she uses a portable heart monitor that records her heart activity at all times. This device should also send her data wirelessly to a central station so her physicians could monitor her regularly. She wants the device to be as user-friendly and small as possible and to be cosmetically-acceptable. She hesitates to have anything implantable due to her age. |

What are some of the needs of the customers?

- • Decoupling cables: In many situations, medical staff, such as Jennifer Grant and Icabod Shahid, are bothered by the amount of cables tied to the patients to collect data. In other words, they would prefer minimized cabling or none to both provide comfort to the patient and to improve ease of device-handling and moving arount patients on their part.

- • Complete solution and programmability: There is a need for devices that come complete (hardware and software) so as to save cost and improve compatibility. In addition to this, there is also a growing demand for system flexibility that allows the device to be usable in a wide range of clinical environmental changes. This means that the device is programmable depending on the user conditions.

- • Modularity and multifunctional: Many medical staff, such as Alicia Stones and Jennifer Grant, prefer using modular monitor that can record multiple vital signals simultaneously from a patient. This reduces staff hours and gives a more accurate diagnosis in the future. The procurement department of hospitals also prefers products that can be upgraded rather than scrapped to cut the costs and space and increase the usability of the products.

- • Remote observation to reduce time between diagnosis and treatment: Current patient monitoring program suffers from one significant disadvantage, that is the patients have to be home-bound. Also, most of the current system does not have cellular capabilities. There is also a demand to reduce or avoid in-patient hospitalization and facilitate patient-care in less expensive settings by improving patient mobility. This is still a partially unmet need for Dr. Brock Jones and Icabod Shahid. Also, there is the launch of American College of Cardiology’s (ACC) door-to-balloon (D2B) time initiative and AHA’s complementary “Mission: Lifeline”. This suggests that if a device is able to send data to medical staff in real time while maintaining patient mobility, it would reduce time between diagnoses and percutaneous coronary interventions (PCI) performed in catheterization labs. As more hospitals strive to meet national guidelines set by these initiatives, demand for wireless ECG solutions will be further boosted44.

- • Portable devices for home-use: The aging American population, like Martina Shingles, are not satisfied with the current solutions because they are not cosmetically-acceptable and do not allow them to move around. Also, she needs to re-charge the device often as it uses much power, that she hopes for a less troublesome device. There is a need by these people for devices that would help in their outpatient care, while still allowing them to lead a normal daily life.

- • Automated irregularities detection: There are times where speed in detection is vital in saving a person’s life, such as in Alicia Stones and Dr. Harie Yacabo’s cases. Devices with increased performance speed and reliability are highly in demand in settings where time is of essence. This need is partially unmet as current manufacturers do not provide very flexible programming for the users and they have lower sensitivity and specification.

- • Clinician-friendly products: Many clinicians, such as Dr. Brock Jones, Dr. Harie Yacabo and Icabod Shahid, see the need for products that are easy to use. This would greatly shorten personnel training hours and reduce time and complexities in procedures. To meet this partially-met need, manufacturers have to work closely with physicians and nurses to understand their concerns, the operational side and design a product that is intuitive for them to use.

- • Data records and viewing: Though traditionally diagnostic devices are valued for their accuracy and reliability, there is a growing need for much more accurate assessment work from the physician’s side via viewing past records. Hence, not only must the devices meet quality requirements, but it also has to address the need of large data recording, tracking, archiving and viewing.

- • Customer support services: Many situations can occur in a hospital setting and the staff have expressed the assurance of having someone to contact regarding device malfunctions or other problems. As such, many appreciate 24 hours/daily customer support services for collaborative planning, training and maintenance.

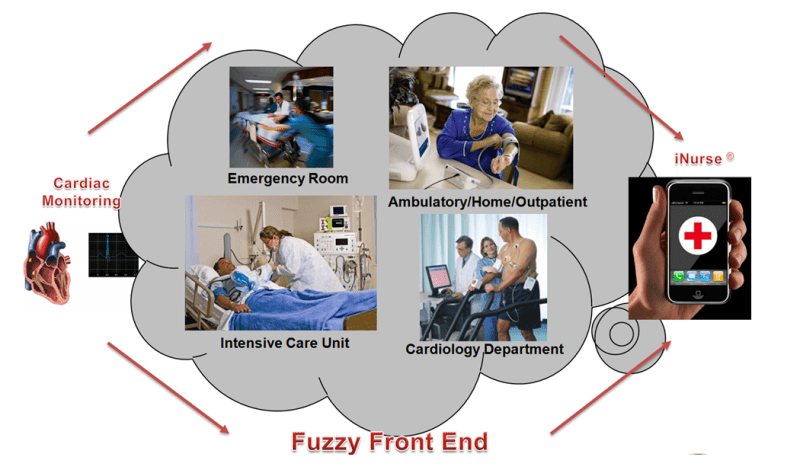

V. The iNurse: Outpatient Monitoring of Cardiac Symptoms

Figure 2. Evolution of iNurse as a solution for cardiac monitoring

Addressing the major needs of Martina Shingles in the home-monitoring/ambulatory segment, we suggest the iNurse! Figure 2 shows the evolution of this solution. The iNurse is a modular, pocket-size device with wireless sensors and minimal cabling. The device can be carried in a patient’s pocket and the wireless sensors are worn on the chest. This design is more cosmetically-acceptable to patients and would not stand out so much in public. We are planning to patent the following features;

- • It is also bluetooth-enabled and is compatible with various mobile devices such as the iPhone and iPad, so that one could view his own data in real-time basis.

- • Cellular network feature allows to transmit data to healthcare providers on a regular schedule and in case of emergencies.

- • The iNurse will have modular capabilities in case the user wants to add more vital signs, such as body temperature and blood pressure.

- • Low power consumption by using body area networking between the device and the wireless sensors.

Although this device was made primarily with the home monitoring segment in mind, development in the future may lead to benefits to the cardiology specialist, ICU, and ambulatory segments.

VI. Micro- and Macro- Industry (Mullin’s part 2)

Teece Analysis

Our proposed solution involves a wireless cardiac monitoring device that connects via bluetooth to a smart phone and then uses the phone’s wireless networking capabilities to transmit data to a physician. We believe that our intellectual asset position is strong. The intellectual asset that we possess is the design to make a small wireless cardiac monitoring device that uses the patient’s skin as a transmitter between the sensors and the device. The major complementary assets we require are; the bluetooth technology to connect our device with a smart phone, the software that allows for our device to be compatible with a smart phone, the physical capital required to manufacture the devices (manufacturing plants), distribution channels, and customer relationships. We believe that the relative cost of acquiring these complementary assets will be low. The bluetooth technology can be acquired through buying a license to use the technology, and the software that allows our device to be compatible with a smart phone can be created in house. The manufacturing plants required to make the devices will require a lot of financial capital to build, however the relative cost of this complementary asset will be medium to low. Distribution channels and customer relationships will be forged through networking relationships provided by our angel investors, venture capitalists, and development team that have experience in this industry. Based on our strong IP position, and relatively low costs of acquiring complementary assets, we believe our venture has strong new business potential. This finding is in accordance with other medical device startups.45

The entrant of the iNurse into the market will shift Porter’s Five Forces as follows;

Buyer Power

We want to provide a decent solution that will shift the buying power from GPO’s or hospitals, to the very end user, the patient. We are creating a product with the end user in mind instead of the prescribing physician, we therefore plan for the demand to be pulled from the patient through the hospital. We want to leverage commodity type products, like cellular phones, to save costs and provide a small cosmetically-acceptable solution. This will be beneficial to health care providers, the payers, and healthcare insurance companies, and the government. This product will be easily promotable through them because it offers three competitive issues (1) reduces inpatient hospitalization which saves a lot of money and increases profitability, especially for insurance companies, (2) facilitates patient care in a less expensive setting, (3) and extends life-expectancy.

New Entrant

We will enter this segment as a new entrant by leveraging the IP we will have on the device features and design patents. As stated earlier, the current high level of interest in wireless cardiac monitor startups makes entering as a new entrant easier because raising necessary capital would be easier.

Industry Competitiveness

Currently, the companies in the manufacturing segment of cardiac monitoring are concerned with consolidation, through mergers and acquisitions, to strengthen their power. This is beneficial as it is a likely option that this company will be acquired by a larger firm, allowing for an easier exit strategy by the founders. If the industry competitiveness is too strong and prevents this manufacturing startup from growing to a size that is attractive to larger manufacturing firms, this startup can transition to a company that focuses on design and IP development.

Solution Positioning Statement: For outpatients (at home or ambulatory) with heart diseases that may be at risk of developing cardiac symptoms, the proposed iNurse device will provide the basic needs of portability and cosmetic acceptability, because it is portable, light, small, wearable, consuming low power and using minimal cabling.

VII. Financials and Venture Analysis

As can be seen from Table 1, an income statement for the venture was formed. In order to build this table, projected revenue level at liquidation, and EBITDA of a proxy company needed to be estimated.

First of all, we assumed that the revenue of our company would be $165 million as the company goes to an initial public offering (IPO) in about 5 years later. CTIA, the international association for the wireless industry, has recently stated the wireless home healthcare market is expected to grow $4.4 billion in 2013, with estimated annual growth rates of 96 percent in 2010, 126 percent in 2011, 95 percent in 2012, and 68 percent in 201346.

Based on this estimation, we project the market size can be up to $9 billion in 2015, and presume that our venture will be able to penetrate 15 – 20 % of the market. This assumption is within the range of CardioNet’s and Volcano’s revenue, $120.45 million and $171.5 million, in 2008, which is less than 2 years from when they went to public. We believe that our venture is comparable to both CardioNet and Volcano as we derive revenue from medical devices, just like them.

Second, EBITDA was computed by taking a proxy company to approximately represent our venture, and by constructing an income statement with the proxy’s data. When it comes to the proxy company for the venture, CardioNet, Inc. (CardioNet) was chosen, because the two companies have shares similarity in that they both produce wireless cardiac monitoring device. Most importantly, CardioNet is considered the only pure-player in wireless healthcare diagnostics industry to have gone public, specifically had an IPO. CardioNet is also one of the few companies to acquire reimbursement from the Centers for Medicaid & Medicare Services, which is very unlikely unless sufficient cost benefits are justified47. The rates for gross profit, selling/general/administrative expenses, and research and development were also adopted from CardioNet; the values of 66 %, 51 %, and 3 % of revenue were used for estimation, respectively. The proxy company shows an EV/EBITDA ratio of 13.23 based on 2008 data (Appendix 1). This is fairly higher than the average of its sector (medical equipment), 8.56 (median = 9.29)48. Therefore, the company is expected to pay back the investment sooner than others. With an assumption of any prediction based on the proxy company’s EBITDA multiples could contain errors, key uncertainties include difference in product types and customers’ response to it, because these may be the major sources of a manufacturing company’s revenue. The company’s financial structure (e.g. costing, accounting, etc.) is also likely to affect the EBITDA multiples, because the numbers in the financial tables depend on which method the company is using to estimate their resources and earning.

The company valuation at liquidation of $260 million was finally estimated and applied to venture financing. A company named Volcano, Corp. (Volcano) was used as our startup example, because Volcano is a player in similar indusry to where our venture is and mature enough for a valuation is performed on. In our references, the IRRs for investors were found as ranges not as specific values. However, all the other data used for constructing the cap tables, including the amount of investment to each round, the length of investment, are reflecting the actual venture investment that had happened to our proxy companies.

The venture investment we planned seems to have a positive return (Appendix 2). They underwent four investment rounds, and each amount per series is reasonably obtained. All investors meet their IRR goals per round with the founders receiving a good $51.21 million (21.2 % ownership) returns at exit. The market capital obtained at exit was strong enough to cover the returns for all investments. The amount of investment at each round decreased as the round went from 2 to 4 at the expense of lower ownership of the founders at exit. Note also that no down rounds were observed, and investment multiples for the investors looked plausible. It is still possible to assign more ownership to investors, since smallest IRRs were not taken in the cap table.

There is a room for making this plan more VC-attractive. For example, if we increase IRRs for round 2 – 4 by 5 percents, the plan would be even more favorable to investors and still maintain as much as 13.6 % for the founders at exit. Or if we could come up with a more efficient procedure to cut costs in SG&A and to maximize operating margin, it could end up having a larger EBITDA with a given revenue. Also, we plan to ensure that the company manufactures a class I or class II product (faster FDA approval), that is compatible with current smartphones or wireless devices and their wireless carriers. This will also improve our chance of attracting investors as shown by recent trends that are direct-to-consumer and quickly adaptable.49 This would hasten the increment curve of our revenue stream and hence our EBITDA and company valuation.

We acknowledge that, in any case, whether or not this venture is VC backable is highly sensitive to the current valuation of the company at IPO/Liquidation. If the company were to be valued at $ 250 million at IPO/Liquidation, then not all investors would be able to meet their investment goals, thus the venture is not VC backable. This difference of valuation is dependent on the projected revenue of the company, a difference of only a couple million in projected revenue. In order to determine whether or not this company is VC backable more extensive research needs to be done to determine a more accurate revenue projection. A more accurate projection could be found by talking to or surveying potential customers and by investigating possible pricing points.

References

1 Frost&Sullivan, CARDIAC MONITORING SYSTEMS MARKET, Mar. 2008

2 Frost&Sullivan, CARDIAC MONITORING SYSTEMS MARKET, Mar. 2008

3 Wikipedia – Cardiac Monitoring: http://en.wikipedia.org/wiki/Cardiac_monitoring

4 Encyclopedia of Nursing and Allied Health: http://www.enotes.com/nursing-encyclopedia/cardiac-monitor

5 OneSource Global Business Browser

6 Angeion Corporation URL: http://www.angeion.com/

7 CASMED, Customer Care, http://www.casmed.com/serviceproduct.html#

8 The health care value chain : producers, purchasers, and providers / Lawton R. Burns, and Wharton School colleagues.

9 North American ECG and Cardiac Monitoring Products Markets, Frost & Sullivan, April 20, 2007

10 CASMED, Customer Care,http://www.casmed.com/serviceproduct.html#

11 Deltex Medical, Clinical Evidence,http://www.deltexmedical.com/clinicaleducation.html

12 CASMED, Customer Care,http://www.casmed.com/serviceproduct.html#

13 Deltex Medical, Clinical Evidence,http://www.deltexmedical.com/clinicaleducation

14 CASMED, Customer Care,http://www.casmed.com/serviceproduct.html#

15 The health care value chain : producers, purchasers, and providers / Lawton R. Burns, and Wharton School colleagues.

16 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

17 http://0-www.medicaletrack.com.lib.bus.umich.edu/TOC.aspx

18 Freedonia Focus on Medical Equipment, August 2009

19 http://www.dicardiology.net/node/29425

20 http://www.dicardiology.net/node/27983

21 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

22 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

23 http://www.dicardiology.net/node/27983

24 Medical eTrack

25 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

26 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

28 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

29 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

30 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

31 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

32 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

33 Medical eTrack

34 “Health Care Equipment and Supplies in the US,” DATAMONITOR, May 2009

35 Medical eTrack

36 Galeon, A. K. 2006, Wall Street’s perspective on medical device evaluation. In: Becker, K. M., Whyte, J. J., Clinical evaluation of medical devices: principles and case studies., Humana Press, 2006

37 The health care value chain : producers, purchasers, and providers / Lawton R. Burns, and Wharton School colleagues.

38 The health care value chain : producers, purchasers, and providers / Lawton R. Burns, and Wharton School colleagues.

39 Stuart, Mary. Is there a Market for Wireless Cardiac Monitoring? Start Up, January 2010.

40 Stuart, Mary. Is there a Market for Wireless Cardiac Monitoring? Start Up, January 2010.

41 IBISWorld Industry Report: Medical Instrument & Supply Manufacturing in the US, March 2010.

42 The Health Industry Value Chain, John Burns and Wharton Colleagues

43 The health care value chain : producers, purchasers, and providers / Lawton R. Burns, and Wharton School colleagues.

44 http://www.dicardiology.net/node/34208/

45 Lecture Slides, Industry Examples as related to Teece, A. Ziedonis 1/2007

46 Wireless Health: State of the industry 2009 year end report, MobiHealthNews

47 Industry Metrics: Wireless Health By the Numbers, pg 20, 2009

48 http://www.infinancials.com/en/market%20valuation,Cardionet%20Inc,42795NU.html

49 Industry Metrics: Wireless Health By the Numbers, pg 18, 2009